Shanghai finally returns to the world today (June 1st). As the center of the whole conflict in the past three months of quarantines, the reopening of Shanghai is a symbol of the end of the most serious round of pandemics in China after March of 2020 and we also take it as the beginning of the wakening domestic demand. Chinese domestic demand has been tepid during the strict quarantines, which has caused great damage to the economy and stainless steel is no exception. Since the lockdown in the middle March, all prices of stainless steel slumped, and inventory keeps reaching high because of the bearish market (Just take at a look at the prices of March 18th). Hopefully, the economy will be back on track. However, there is a view that it won't take effect in the stainless steel market that soon because the spot inventory is too large. But to our oversea buyers, it means the opportunity is still waiting. The point is that, don't let it wait too long because it will pass. About the decreasing prices, spot and futures inventory, and the price forecast, please keep rolling and read the full Stainless Steel Market Summary in China.

WEEKLY AVERAGE PRICES

|

Grade |

Origin |

Market |

Average Price (US$/MT) |

Price Difference (US$/MT) |

Percentage (%) |

|

304/2B |

ZPSS |

Wuxi |

3,180 |

-39 |

-1.27% |

|

Foshan |

3,225 |

-39 |

-1.25% |

||

|

Hongwang |

Wuxi |

3,100 |

-33 |

-1.10% |

|

|

Foshan |

3,075 |

-57 |

-1.91% |

||

|

304/NO.1 |

ESS |

Wuxi |

3,020 |

-51 |

-1.74% |

|

Foshan |

3,055 |

-39 |

-1.32% |

||

|

316L/2B |

TISCO |

Wuxi |

4,830 |

-23 |

-0.48% |

|

Foshan |

4,840 |

-33 |

-0.70% |

||

|

316L/NO.1 |

ESS |

Wuxi |

4,530 |

-63 |

-1.42% |

|

Foshan |

4,575 |

-51 |

-1.14% |

||

|

201J1/2B |

Hongwang |

Wuxi |

1,690 |

-45 |

-2.80% |

|

Foshan |

1,670 |

-60 |

-3.75% |

||

|

J5/2B |

Hongwang |

Wuxi |

1,580 |

-48 |

-3.19% |

|

Foshan |

1,575 |

-62 |

-4.07% |

||

|

430/2B |

TISCO |

Wuxi |

1,550 |

-15 |

-1.04% |

|

Foshan |

1,525 |

-24 |

-1.68% |

TREND|| Prices keep decreasing. Signs show that the prices will be steady.

From May 23rd to May 27th, the spot price of stainless steel continued to decrease. The domestic market continues to be bearish. Buyers are more cautious when the prices were decreasing. As of May 27th, the most-traded contract of stainless steel rolled over, and the price dropped by US$119/MT to US$2,885/MT compared to the price on May 20th. The base price difference between spots and futures widened to US$221/MT, which increased by US$74/MT.

300 series of stainless steel: Prices of spots and futures are weak.

Last week, both spots and futures prices decreased. Until May 27th, the base price of cold-rolled stainless steel 304 of private-owned mills in Wuxi declined by US$45/MT compared to the price of May 20th, reaching US$3,035/MT. As for the hot-rolled stainless steel 304, the mainstream quotation was down by US$60/MT to US$2,990/MT. The drop in price did not attract buyers’ extra attention. In the afternoon of May 27th, due to the boost in nickel price, the sluggish market was finally wakened and transactions increased slightly.

The major materials of stainless steel 304 has decreased after the May holiday. The EXW price of high-grade ferronickel dropped by US$6/Ni US$233/Ni, and the price of ferrochromium remains at US$1,436/50 base tons.

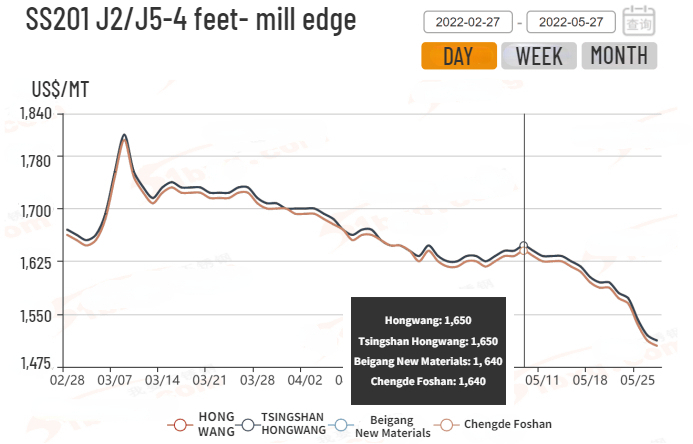

200 series of stainless steel: The price slumps by US$158/MT in 20 days.

Over the last week, the spot price of stainless steel 201 in Wuxi remained the declining tendency. Until May 27th, the base price of cold-rolled mill-edge stainless steel 201 decreased by US$45/MT to US$1,640/MT; as for the base price of stainless steel J2 and J5, that of mill edge even decreased by US$60/MT, to US$1,520/MT. About the 5-foot hot-rolled stainless steel 201, the price was reduced by US$30/MT, hitting down to US$1,680/MT.

The trading situation was poor as weeks before under the pessimistic sentiment in the market. The prices of stainless steel keep breaking down new low, take the cold-rolled stainless steel J2 as an example. On May 9th, the price of CR J2 was US$1,650/MT which was a recent record high price and on May 27th, it went down to US$1,490/MT. A decrease of US$160/MT, down by 10.3% within 18 days, which is astonishing to us.

400 series of stainless steel: Oversupply makes the decrease in price difficult to change.

Last week, the cold-rolled stainless steel 430 decreased slightly. Until May 26th, the mainstream quotation of cold-rolled stainless steel 430 in Wuxi was US$1,545/MT which decreased by US$23/MT compared to a week before. Last week, TISCO and JISCO ‘s guidance price of CR stainless steel 430 dropped by US$30/MT, reducing to US$1,685/MT and US$1,670/MT respectively.

The cost of raw materials might drop in the future as the high chromium production returns to normal after the overhaul. It is predicted that the production of high chromium in May increases by around 620,000 tons which are 30,000 tons higher than that of April. According to the customs data, the import of ferrochromium in April is 203,500 tons, MoM rising by 10.46%.

Summary:

300 series of stainless steel: The quarantines and pandemics are hopefully coming to end. China is undertaking huge economic pressure, and thereby, the overall recovery in all industries and businesses is bringing out. The domestic demand for stainless steel is gradually increasing. Last week, the nickel price increased and it boosted the stainless steel market and confidence. The stainless steel prices have suffered from the continuous decrease. It is predicted that the stainless steel prices will tend to stop reducing and be stable.

200 series of stainless steel: So far, the market remains weak. The inventory is high, so there has nothing to prop up the stainless steel prices. However, the prices are also difficult to decrease because the costs are high in both the ranges of production and operation. In the short term, there is not much room for the stainless steel prices to reduce. It is predicted that the price of stainless steel 201 will fluctuate weakly. The CR SS201J2 coil will remain above US$1,475/MT.

400 series of stainless steel: In Wuxi, TISCO and JISCO quoted US$1,545/MT ~ US$1,550/MT for stainless steel 430/2B, which dropped by US$23/MT. According to a source in the industry, the pressure of the high spot inventory remains and traders have to give discounts, and some of the prices went down to US$1,520/MT. But as JISCO starts the overhaul plan, the production of stainless steel 400 series will reduce. Considering that the latest bidding price of high chromium from TISCO and TSINGSHAN in June remains the same as last month, which props up the cost of the stainless steel 400 series. It is predicted that the price of stainless steel 430/2B will remain weak but stay above US$1,520/MT.

FUTURES|| ShFE nickel might fall after rushing high.

"On May 24, Indonesian Investment Minister, Bahlil stated that Indonesia will ban the export of nickel products with a content of lower than 50%. Furthermore, The Ministry clarified that there is a plan to impose export duties on processed goods with a raw material content of less than 70%. On the same day, the nickel price on Shanghai Futures Exchange opened high and went up even higher. It closed at UD$31,741/MT, which increased by US$1,147/MT, and the rising percentage was 3.75%. LME nickel also opened to rise. But on May 25, LME nickel dropped by US$1,295/MT to US$26,485/MT, and the most-traded contract of ShFE nickel decreased by US$678/MT to US$30,695/MT. However, the contract for June of stainless steel futures rose by US$18/MT, to US$2,935/MT."

About Shanghai Futures Exchange Nickel:

The main contract of Shanghai Futures Exchange Nickel, the stock price once dropped below CNY200,000 (US$30,075). Stimulated by the news of Indonesian export duty on nickel products and the low inventory, the nickel price jumped above CNY210,000 (US$31,579).

About the nickel ore, the price last week was steady although the ferronickel price decreased and the supply from the Philippines will increase soon, which attracts ferronickel producers’ sight and they are waiting for the nickel ore prices to fall. It is predicted that the price of nickel ore will reduce.

Speaking of ferronickel, influenced by the sluggish demand for stainless steel and decreasing stainless steel production, the price dropped to US$236/Ni. It is predicted that the price of ferronickel will remain weak. The refine nickel is low in inventory both in Chinese domestic and global markets. The inventory of the Shanghai Futures Exchange fell to a record low, to 1,200 tons and the LME nickel inventory is 72,200 tons. The supply is increasing, but it is at a low level and still supports the nickel price. From a macro perspective, FED will keep raising the interest rate, the tightening short will again drag down the market.

The conclusion is that the nickel ore and ferronickel will reduce in price influenced by the gloomy stainless steel market and the refined nickel will remain high as long as the inventory is low. It is predicted that the price of ShFE nickel will probably rush high and fall back down.

About stainless steel futures:

From May 23rd to May 27th, the main contract of stainless steel futures price was weak and fluctuated. Although the nickel price rose, the stainless steel market did not move with the increase instead, it kept falling.

What brings to the feeble situation is that the raw material cost has reduced. Some steel mills reduced their production because of the gloomy market, stacking inventory, and high cost of materials. The decrease in steel production causes less demand for ferronickel and ferrochromium and thus the prices are reduced. However, to the current historically low prices of stainless steel, the raw material cost is rather high. Steel mills might keep exploring more margins by squeezing the material cost.

In a short term, the stainless steel market will remain gloomy because the market needs time to recover although the pandemic is under control and Shanghai reopens on June 1st. Unlike an announcement that is brought to the society immediately, consumption and market confidence will follow behind only when people and their activities move around. Another reason is that the market inventory is oversaturated which has accumulated in the past two months. It also takes time to digest the oversupply.

To sum up, due to the oversupply, large inventory, and decreasing cost, the price of stainless steel futures will remain weak and fluctuate in a short term.

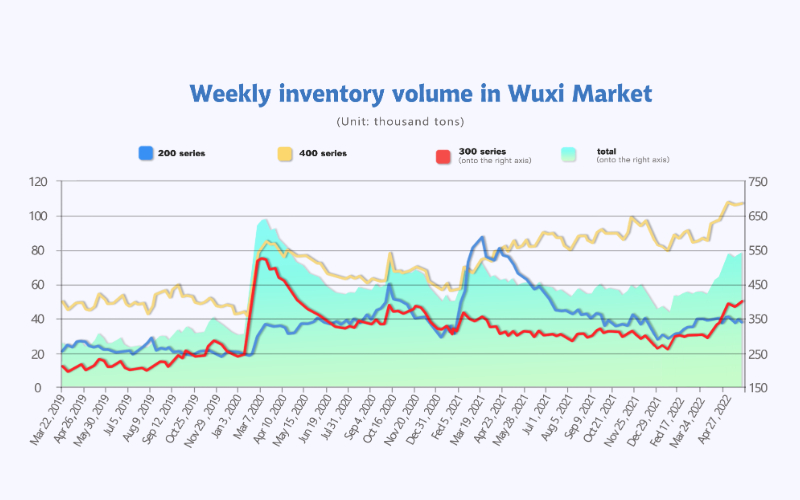

INVENTORY|| Spot product continues to increase and trading remains feeble.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| May 19 | 38,996 | 388,243 | 105,493 | 532,732 |

| May 26 | 37,351 | 397,739 | 106,307 | 541,397 |

| Difference | -1,645 | 9,496 | 914 | 8,665 |

Last week, the inventory volume in the Wuxi sample warehouse continue to increase from 532,700 tons to 541,400 tons, rising by 8,700 tons. 200 series inventory decreased by 1,600 tons, to 37,400 tons; 300 series increased by 9,500 tons, to 397,700 tons; 400 series increases by 800 tons to 10,630 tons.

200 series of stainless steel: Steel mills’ on-way resources reduce.

The 200 series inventory of Wuxi dropped by 1,600 tons to 37,400 tons and the decrease mostly comes from the on-way resources, the pre-stock products in Jiangyin where it was locked down. The new arrivals were mostly from Baosteel Desheng, and about 2-ships of products were shipped to Wuxi. So far, both cold-rolled and hot-rolled stainless steel 201 are adequate.

300 series of stainless steel: The weakness of transaction and the increase of stock remain.

Last week, because the on-way resources of steel mills increased, the inventory of 300 series in Wuxi rose. Shanghai reopens on June 1st, which is a sign of the recovery from this round of pandemics in China. The logistic has improved, and products are shipped without any problem, but the biggest problem is the poor demand which makes the stock stacked. It is afraid that if the demand fails to recover soon, the newly added capacity will take effect into the stock in the second half of the year and the inventory will keep increasing.

The price of futures decreased, while the spot price increased. The price difference between spot and futures widens to US$230/MT. Buying warehouse receipts is preferable compared to spot products. Until May 25th, the futures inventory of the Shanghai Futures Exchange was 28,900 tons which have reduced by over 50,000 tons from the peak in April.

400 series: JISCO’s overhaul will hopefully reduce the high inventory.

Last week, the inventory of 400 series rose slightly by 800 tons to 106,300 tons due to the low demand. But it is predicted that the inventory will decrease because JISCO has started to overhaul and stop producing.

NICKEL: Indonesia to ban exports of processed products with nickel content below 50%.

Recently, Indonesia has mentioned restrictions on the export of nickel products. On May 24, Indonesian Investment Minister Bahlil Lahadalia said that Indonesia will ban the export of nickel processed products with a content of less than 50%, aiming to increase added value.

He added that Indonesia will no longer allow the export of processed products with nickel content below 50%, and it must be 60-70%. The government will focus on nickel for the car battery ecosystem, and several companies are already investing in the industry.

Indonesia banned the export of nickel ore on January 1, 2020. Since then, there have been rumors about restrictions on the export of nickel products coming out.

According to Bloomberg in September last year, Indonesia may set limits on nickel exports, restricting the export of nickel products with a content of less than 40%.

There is also news that Indonesia is discussing export taxes on products with nickel content below 70% to drive the development of the local refining industry. Stimulated by this news, LME nickel futures once surged 4.5%.

If Indonesia bans the export of processed products with a nickel content of less than 50%, it will have a significant impact on China's ferronickel supply.

According to customs statistics, in April 2022, China imported a total of 419,100 tons of ferronickel, of which 390,500 tons of ferronickel were imported from Indonesia, accounting for 93.18%; From January to April, China imported a total of 1.5655 million tons of ferronickel, and 1.3993 million tons of ferronickel from Indonesia, accounting for 89.38%.

Some said that it is more like "hype" since there is no official announcement at present, nor a specific implementation time either.