COVID-19 remains in China. Shanghai the metropolitan has gotten stuck in the pandemic for more than one month, and the lockdown has lasted for 11 days since March 28th. This is the turbulence inside China, while outside of China, the backlash of the war is conveyed in China in an economic way. Both of the biggest troubles give a punch to China's economy in March. Stainless steel prices fluctuate, facing increasing material and additional costs as well as weak demand. From March 28th to April 1st, the prices tended to drop and were maintained. The prices seem to remain to fluctuate for a while before the pandemic inside China can finish somehow the authority approves. But who knows when. If you want to know more about the PMI analysis of the Chinese market and the stainless steel prices, please keep reading our Stainless Steel Market Summary in China.

|

Grade |

Origin |

Market |

Average Price (US$/MT) |

Price Difference (US$/MT) |

Percentage (%) |

|

304/2B |

ZPSS |

Wuxi |

3,510 |

10 |

0.28% |

|

Foshan |

3,560 |

10 |

0.28% |

||

|

Hongwang |

Wuxi |

3,400 |

-13 |

-0.39% |

|

|

Foshan |

3,350 |

-62 |

-1.90% |

||

|

304/NO.1 |

ESS |

Wuxi |

3,305 |

-22 |

-0.70% |

|

Foshan |

3,350 |

-37 |

-1.13% |

||

|

316L/2B |

TISCO |

Wuxi |

5,145 |

-13 |

-0.25% |

|

Foshan |

5,155 |

-29 |

-0.57% |

||

|

316L/NO.1 |

ESS |

Wuxi |

4,915 |

-60 |

-1.25% |

|

Foshan |

4,960 |

-60 |

-1.24% |

||

|

201J1/2B |

Hongwang |

Wuxi |

1,925 |

-24 |

-1.31% |

|

Foshan |

1,940 |

-14 |

-0.78% |

||

|

J5/2B |

Hongwang |

Wuxi |

1,810 |

-10 |

-0.56% |

|

Foshan |

1,835 |

-21 |

-1.20% |

||

|

430/2B |

TISCO |

Wuxi |

1,695 |

0 |

0 |

|

Foshan |

1,675 |

-5 |

-0.31% |

TREND|| Market locks down and prices reduce.

From March 28th to April 1st, the stainless steel spot price decreased at the beginning and then started to maintain. Last week, influenced by the quarantine regulations, the Chinese market was weakening. Some small increases appeared with the fluctuating nickel and stainless steel futures price. However, with more steel trading markets have been locked down, the transaction almost dropped to stop. Until last Friday, April 1st, the main contract of stainless steel futures went down by US$148/MT, to US$3,365/MT. With the falling futures price, the gap between the spot price and futures price widens to US$94/MT, up by US$84/MT compared to March 25th.

300 series of stainless steel: Delivery continues to be postponed.

Over the last week, the spot price of stainless steel 304 was stagnant. Earlier in the week, as stainless steel futures price kept falling, the price of stainless steel spot gradually decline. In the later week, because Wuxi takes harsh measures against the pandemic, the delivery has been blocked. Many traders said that they are open to new orders but the delivery time is unsure. Until April 2nd, the base price of the cold-rolled stainless steel 304 of private-owned mills dropped by US$48/MT, to US$3,385/MT; the price of hot rolling was down by US$79/MY to US$3,305/MT. About the transaction, it was getting warm when the prices decreased, but when the quarantine regulations tightened, the transaction was turned down again.

Though the price of high-grade ferronickel reduces, and the ferrochrome price remains, the production cost of stainless steel decreases in theory. However, afraid that steel mills are short on raw material stock, future production might be affected.

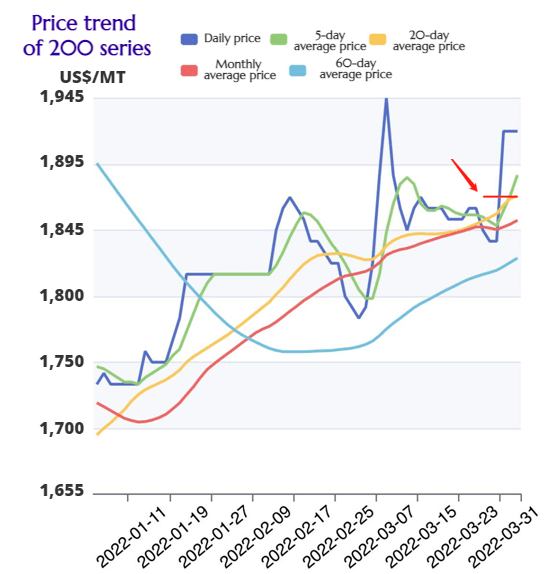

200 series of stainless steel: As markets lock, the transaction dives.

Last week, the stainless steel 201 was bland in trading due to the continuous lockdowns of various steel markets and logistic parks.

The cold-rolled stainless steel 201 reduced by US$24/MT to US$1,885/MT. Stainless steel 201J2 fell by US$247/MT as well, to US$1,775/MT. As for the hot-rolled 5-foot stainless steel dropped by US$16/MT, to US$1,895/MT.

The price of stainless steel 201 was also restricted by the quarantine. Monday night, a steel market was suddenly locked down. All the traders have to work from home and some even choose to have a rest. More and more markets were closed, making the stainless steel spot trading get stuck in paralysis. In this case, traders tended to maintain the quoting price instead of decreasing the price.

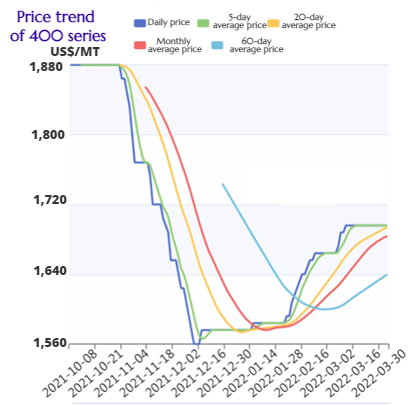

400 series of stainless steel: Pandemic limits the demand but the high cost remains.

The price of cold-rolled stainless steel 430 in Wuxi market remains at US$1,695/MT, the same as last week.

The cost of high chromium remains the most influential factor in the price of the stainless steel 400 series. Although the output of high-grade chromium increases significantly, the cost can’t reduce due to the expensive chromium ore. It is expected that the output of high-grade chromium increases greatly by 600,000 tons.

Summary:

300 series of stainless steel: The whole industry suffers from quarantine. In a short term, steel mills face not only fewer orders but also a high cost of raw material, which will result in low supply in April. Meanwhile, the demand for stainless steel is declining amid the pandemic. The weak supply and demand will remain for a while and the price will keep fluctuating, above US$3,275/MT which is a production cost point.

200 series of stainless steel: Almost all industries suffer from the new round of COVID-19. Stainless steel traders take the opportunity to maintain the price and stop the decreasing intend. In a short term, the price of cold-rolled stainless steel 201J1 will remain at around US$1,880/MT. What we are hoping for is an effective control and the settle-down of the pandemics, after which, the logistic system, as well as demand and supply, will recover.

400 series of stainless steel: In the Wuxi market, stainless steel 430/2B of TISCO and JISCO were quoted at around US$1,700/MT, the same as last week. Though the transaction is quiet, suppliers held the price because the purchasing price of high-grade chromium rose by US$72~US$79, making the cost of raw material keep increasing. In a short term, with the rising price of ferrochromium added to stainless steel, it is predicted that the price of stainless steel 430/2B will grow slightly to US$1,710/MT. The price will fluctuate between US$1,660/MT and US$1,720/MT.

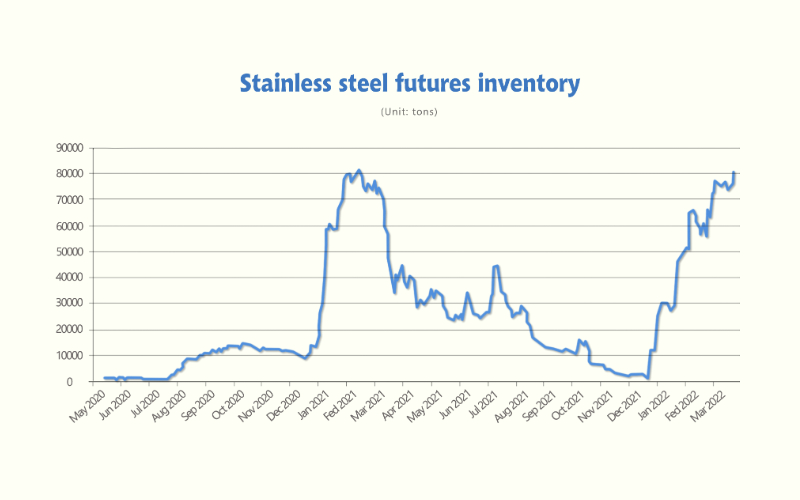

FUTURES|| Market is sluggish both on the demand and supply side.

Until March 31st, the warehouse receipts in Shanghai Futures Exchange is 80,721 tons, increasing by 6,928 tons compared to March 24th, which is very close to the highest in 2021, which was 81,264 tons. On March 30th, the contract for May of stainless steel futures increased by US$83/MT to US$3,440/MT, but on the next day, it soon fell down to US$3,340/MT.

The main contract of stainless steel futures fell back earlier last week, then maintained at US$3,320/MT. Last week was close to the Qingming Festival in China, which made the price trend less fluctuating. The high cost of raw materials has leveled up the stainless steel stock price until now. What’s worst, the quarantine regulations have postponed the delivery, resulting in a feeble supply and demand. But based on the high cost, the price will remain high and fluctuate.

However, the price is difficult to keep rising. The reasons are: first, demand won’t recover and increase until the new round of breakout of COVOD-19 in China is settled down. The regulation levels up and the uncertainty in the market is also increasing. Second, the inventory in steel mills might be stacked due to the blocking logistics and weak demand. Once the inventory rushes out, the stainless steel prices will crumble. The sluggish market might only recover when the logistic returns to normal.

To sum up, because the raw materials remain high in price, the stainless steel price will hardly run beyond US$3,160/MT ~ US$3,320/MT. If the demand remains low, stainless steel prices will probably go down.

INVENTORY|| Inventory reduces when the market locks down.

| Inventory in Wuxi sample warehouse (Unit: thousand tons) | 200 series | 300 series | 400 series | Total |

| March 21st ~ March 25th | 38.9 | 300.4 | 85.8 | 425.1 |

| March 28th ~ April 1st | 39.4 | 294.2 | 85.3 | 418.9 |

| Difference | 0.5 | -6.2 | -0.5 | -6.2 |

Last week, the inventory volume in the Wuxi sample warehouse decreased by 6,200 tons, to 418,900 tons. 200 series inventory reduced by 500 tons, to 39,400 tons; 300 series declined by 6,200 tons, to 294,200 tons; 400 series decreases by 500 tons to 8,530 tons.

200 series of stainless steel: A stainless steel market closed down for one week, and transactions dropped.

On March 29, Eastern steel market in Wuxi was locked down and more steel markets followed suit later on. Baosteel Desheng kept delivering products to the spot market. The spot transaction cooled down greatly, and the inventory of 200 series increased slightly by 500 tons.

300 series of stainless steel: Inventory reduced as the traffic is blocked.

Due to the quarantine policy in Wuxi, the products are difficult to reach the market and thereby the inventory volume fell by 6,200 tons to 294,200 tons. On March 31st, the cold-rolled stainless steel 304 once dropped below US$3,320/MT, attracting some buyers to stock up. The transaction slightly rose.

400 series of stainless steel: Products are hard to get in and out.

It is expected that the output of 400 series in March increases by more than 90,000 tons, to 556,500 tons. As for the inventory in the Wuxi sample warehouse, it was slightly reduced by 500 tons to 85,300 tons. Due to the blockage of traffic, the trading volume has been low, resulting in high pressure on the inventory.

MACRO|| China Manufacturing Activity Slumps to Two-Year Low

The recent pandemic has caused some recession to China’s manufacturing industry. On March 31st, National Bureau of Statistics of China released that, in March, the Purchasing Manager Index (PMI) of China's manufacturing industry was 49.5 percent, down 0.7 percentage point from the previous month, lower than the threshold, and the overall prosperity level of the manufacturing industry fell somewhat. ( PMI index below 50% reflects a recession.)

According to an analytic, Sun Yongle, COVID-19 is the main factor causing the weakening of the manufacturing sector. Since March, the new round of the pandemic has had a significant impact on China’s production and consumption. Affected by this, the short-term domestic economy has dropped significantly. He said that in addition to the pandemic, the geopolitical conflicts between the two energy giants have led to increased pressure on imported inflation, and the rising prices of some raw materials have also influenced on the production of industrial enterprises.

EXPORT DILLEMA 1 -- PRICE INDEX KEEPS INCREASING

The geopolitical conflict exacerbates the pressure on China's imported inflation. The two energy giants worsen the intense supply of the commodity. In March, crude oil, nickel, aluminum, corn, and other important products have fluctuated and risen significantly.

How the influence effect the market is that the main material purchase price index and producer price index both increase to 66.1% and 56.7% respectively, which is 6.1% and 2.6% higher than in February. Facing the increasing material cost and tepid demand, the manufacturing material inventory index also falls down by 0.8% from last month to 47.3%. Besides the inflation, the war also brings uncertainty to much Chinese export business. Chinese suppliers are more cautious in developing international business. Due to the war, the order is reduced and some are even canceled. Reflecting on the data, the new export order index dropped by 2.8% compared to February, down to 47.2%.

Relating to the stainless steel industry, the purchase price index and producer price index of the main raw materials such as petroleum coal and other fuel processing, ferrous metal smelting and rolling processing, non-ferrous metal smelting and rolling processing, etc. both exceeded 70.0%.

According to the vice president of financial information research institute, Wu Chaoming, he believes that the PMI in future months will stay above 50%, and the manufacturing industry will recover.

EXPORT DILEMMA 2 – TRANSPORTATION IS OF LOW EFFICIENCY

The back and forth of the pandemic in China is another key factor that reduces the new order index.

We have kept mentioning that the latest pandemic is the most influential and after the first time we faced COVID in 2020. It is fatal because two major cities in China, Shenzhen and Shanghai fell into the breakout of COVID-19 one after another. To deal with the pandemic, the two large cities began to lockdown and the surrounding cities also held strict quarantine measures. Until now, Shanghai is still having paused. Shenzhen and Shanghai are two important port cities and export cities. Some of our orders are also arranged to be shipped out from these two ports. When the cities shut down, business stop, as well as transportation, is suspended.

The supplier delivery time index in March is 46.5%, MoM reduces by 1.7%, which hits the lowest since March of 2020.

Shanghai and Shenzhen are important ports in China. In 2021, the container throughput of Shanghai Port and Shenzhen Port will account for about a quarter of China's total throughput.

Although the quarantine does not close the port, to align with the regulations, truck transportation, and ship operation have been affected. Major ports such as Yantian Port and Shanghai Port have experienced congestion. According to Refinitiv ship-tracking data, there were about 34 ships waiting to dock off the coast of Shenzhen when the outbreak was severe, while a year ago, the number was 7.

Meanwhile, the finished products inventory index rose to 48.9%, MoM increasing by 1.6%.

The pandemic intensifies the downsize of demand and supply. On March 29th, from China’s state council, the government will take much to lead and boost the economy, such as by investing in infrastructure. And almost all experts foresee that governmental investment will be carried out soon.

However, to us, the most urgent problems are the high material price and the insufficient transportation.

Until now (April 8th), Shanghai has confirmed nearly 130,000 positive cases, and the lockdown is prolonged until the authority considers it is time. Many Chinese suppliers share the same dilemma as us—— some of our products are difficult to find a way to the ports, and meanwhile, the raw material cost and other additional cost is increasing.